Here’s something you probably didn’t know.

NETS is equally owned by Singapore’s three largest banks.

It’s also why there was a bit of a confusion as the various banks started introducing their own version of the QR codes in 2020, when COVID happened.

Were they cross competing?

But things are a little clearer now with SGQR, the QR system that aims to unite the various QR types amongst the different banks.

But it’s easier said than done.

If you’re a merchant

You might be a business owner thinking of implementing PayNow QR, but you’re at a loss at what option is actually better.

| NETS QR | SGQR, offered by the 3 local banks (OCBC, DBS and UOB) | |

|---|---|---|

| How to get started | Fill up the application form, and then scroll to the bottom of this page, and click “Apply for SGQR Label Online” | Apply through the banks business banking apps |

| Ease of application | Not easy, especially when you look at the form below | DBS is relatively easy, and was done within 5 minutes on DBS IDEAL |

| Fees for application | No fee | No fees |

| Transaction fees | 0.8% per transaction | 0%, for now for DBS, UOB, and OCBC But if you want to see the instant notification, you need to set up DBS Max, which charges 0.25% per transaction. For UOB mCollect, there’s a 0.15% per transaction fee for now. OCBC One Collect charges 0.25% per transaction after the first 3 months. |

| Payment confirmation | You get to see it immediately through the NETS Biz app on your phone. | The payment (at least for DBS, which I use) is consolidated and only comes through at the end of the day. |

Ease of application

Let’s just start with the ease of application. If you look at the application form below, you can quickly see yourself face-palming, wondering how you’re going to get through this form.

There’s a secret hack though.

Just do it through your local bank’s business banking app.

Through DBS Ideal

Doing this through DBS IDEAL was easy.

DBS liaised with NETS and sent a NETS guy to follow up with me.

This NETS guy went to quite some distance with his customer service, coming down to my office, offering to meet me wherever was convenient.

He almost met me whilst I was on a date in City Hall, because it was where he was.

But you get the idea.

Doing it through the bank, which then outsources it to their vendor in NETS, allows you to save time.

When he eventually met me, he gave me the forms, and then let me sign them.

In 4 weeks, he arranged to meet me again to pass me the laminated QR codes, and taught me how to use the NETS app.

It’s not without reason.

The NETS app does take a transaction fee.

Through OCBC

For example, OCBC shares an easy guide you can do it here.

Both the app and the business banking page will work.

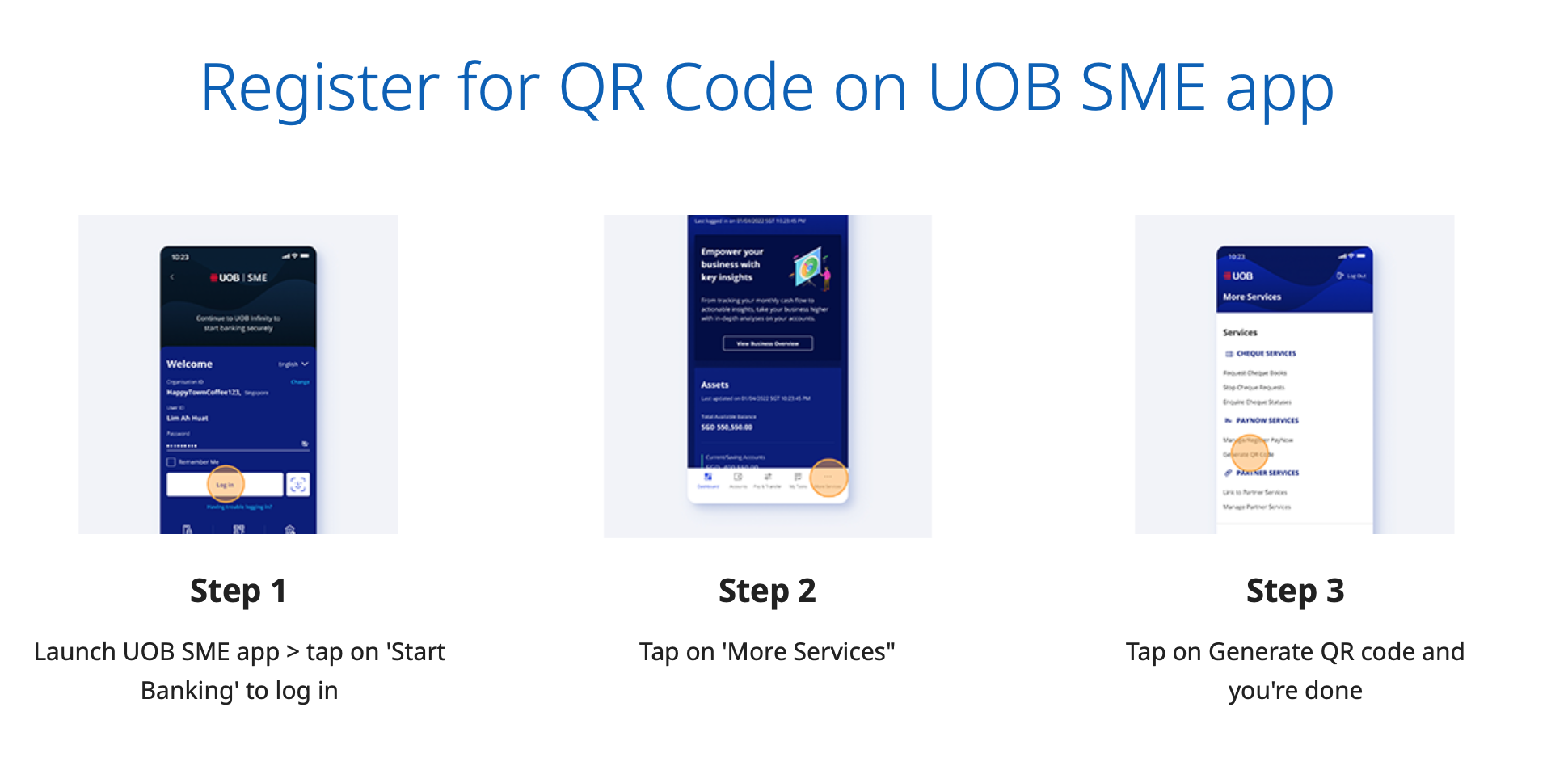

Through UOB

If you’re with UOB, you can register for your QR code through the app. You can check this page for a more detailed explanation.

After that, you get your first print of labels for free.

With UOB, you also have something similar to the NETS Biz app, when you receive the instant notification of payment.

They also do not charge you for the transaction fee (until end 2025, though whether they will extend it remains to be seen).

Transaction fees

Personally I don’t think the fee that NETS takes is that big. It’s 0.8%, per transaction.

But given that it is per transaction, and that most small businesses would go by volume, (think of your meepok uncle selling hundreds of bowls everyday) rather than value, it may add up.

Let’s compare this to not using the NETS QR.

You will get the update on the sales you got only at the end of the day.

For the peace of mind

If you want to see whether your customer paid, the fastest way seems to be through the NETS QR code, which directly integrates into your NETS Biz app, allowing you to see an immediate readout of the payment made.

Try your local bank first

There is a nuance here.

Whilst NETS might be the well known name in the industry, it’s clear that they charge more than all the 3 banks.

For me, I’ve overcome it by not using any of the collection methods (like DBS Max, or OCBC One Collect). I’ve just made sure that the person has paid by looking at their phones closely.

I know – it’s not ideal. But for context, I’m not primarily collecting through in-person, but mostly through direct bank transfers.

You might have a storefront where most people pay to you.

In that case, you might want to use NETS because they have an excellent customer service that goes to you, rather than you having to set it up on your own.

But if you’re doing high volumes of transactions everyday, just be sure that you mark in the 0.8% as an added cost.

It’s not little, but if you’re doing $500 of sales through NETS QR a day, that $5 over 30 days does add up to a $150 per month.

Struggling to implement?

Of course, if you’re struggling to implement your PayNow or POS methods, you can always speak to us. We are more than happy to help. Contact us here.